Define FBN’s First Finance Customer Archetypes

My Role:

Organized and facilitated cross-functional workshops and meetings to ensure team alignment on timelines, plans and goals.

Conduct interviews and led focus groups to collect user insights

Led and facilitated synthesis workshops where the team distilled research into archetypes that informed design decisions, ensuring the final product aligned with user needs.

Project Highlight:

Inform finance project planning and design directions by leveraging user insights and research outcomes

These archetypes became the foundation for product definitions and design solutions, guiding the development of features tailored to users’ needs

Team

1 UX Researcher | 2 PMs | 2 Designers

Additional support from the Farmer-2-Farmer conference for focus groups.

Project Timeline

Oct 2022 Oct - Feb 2023

Quick Links:

Research Context

We realized that while we had built some core features, our knowledge of customer needs was lacking, especially in the finance department. These insights are crucial for guiding product definition and design directions, so to bridge this gap, we conducted generative research to better understand our users’ needs, challenges and overarching goals.

By collaborating with product, design, business and marketing teams, I helped guide the research process through:

Kick-off Workshops: Brainstorming sessions to identify gaps in our knowledge and aligned teams on research priorities.

Interview Coordination: Go over interview policies, aligning teams on do’s and don’ts, and debriefing after each session.

Synthesis Sessions: Workshops to turn raw research data into key archetypes, and actionable insights.

Why Archetypes not personas?

In this project, we chose to develop customer archetypes instead of traditional personas. Archetypes allow us to focus on underlying behaviors, motivations, and goals that are shared across different customer segments. This was crucial in the financial space, where users' goals and actions are more indicative of their needs than superficial traits like age or occupation

Archetypes provided a more holistic and flexible framework, enabling our teams to focus on core behaviors and decision-making patterns that drive customer actions.

Using archetypes allow us to design for broader behavioral patterns, ensuring that our solutions were adaptable across different user types without being tied to specific demographics.

Research Goals

During the kick-off workshop, we reviewed our existing knowledge, identified gaps, and established the primary goal and key research objectives:

Primary Goal:

Gain a holistic understanding of our users so that we can improve and build products that better align with their needs and metal models.

Key Research Objectives:

Identify main customer archetypes attracted to our products.

Understanding users’ key challenges and successes in securing loans (not limited to our loan product)

Understand users’ overarching goals for their operations and the role loan plays in achieving them.

These insights would inform our platform strategy, helping us create a more user-centered experience. In the longer term, we aimed to increase conversion rates, reduce bounce rates on key pages, and decrease customer support touchpoints.

Research Methodology & Process

Methods:

1-on-1 interviews on the farms & online, focus groups during the F2F conference.

Recruitment:

We collaborated with the loan team to recruit a mix of users and non-users from key agricultural regions across the U.S. to ensure diverse perspectives.In total, we recruited xx participants, the research involved a combination of remote and in-person interviews to accommodate participants’ preferences and availability.

Interview Guide and Script:

Interview Discussion Guide: Link

Some Images From the Research:

Driving to a customer’s farm in Kansas for the interview

It was feeding time right after an interview, and the farmer asked if we wanted to feed the lamb!!!!!

The awesome team that helped with focus groups during the conference

Data Collection & Synthesis

After conducting the interviews and focus groups, the ux researcher and I compiled the data into themes to identify common patterns and outliers. Once we had a preliminary outline of the different customer types, we gathered all key stakeholders in an online session to review the findings and ensure alignment across teams.

To finalize the archetypes, I facilitated a brainstorm workshop where we collaboratively generated names for each archetype. We then used dot voting to select the final names. It felt good to see the abstract concepts take shape, giving everyone a clearer picture of who our customers are.

See the research Insights below👇

The research findings have helped us build the roadmap and become the guiding pillars for a lot of design decisions. Here are some examples.

Jump to…

Impact of the Research

Enable Easier Access to Funds

Research Findings:

Farmers across all four archetypes expressed frustration with the slow operating line process, especially in time-sensitive situations like cattle auctions or co-op discounts. The delay in accessing funds added stress and hindered their ability to act on opportunities.

What We Did:

We streamlined the fund request process by digitizing bank account linkage and fund request process, eliminating the need for DocuSign, reducing the time to access funds from 5 business days to 2.

Impact:

Reduced fund access time from 5 business days to 2, improving farmers’ ability to act on time-sensitive opportunities.

Setting up Direct Deposit

Before: A docuSign form is emailed to the farmer and the loan team needs to manually verify the bank info, it takes up to 5 business days.

After: Farmer can link their bank account on FBN app under 3 minutes

Request Draws

Before: Farmer needs to fill out a DocuSign everything they need access to the fund, loan team needs to manually review it, it often was processed late during the busy season.

After: Farmer can now request draws through their app using a simplified digital form, anytime and anywhere.

Digital Payment Capability for Farmers

Research Findings:

Without surprise, farmers encountered problems with the paper check repayment systems, leading to delays and additional interest charges:

Mail person lost checks took over a week to notice, resulting in late payments

Farmers wrote inaccurate amounts, leading to the need to send extra checks or for FBN to return additional amounts with a check.

Concerns about mailing large amounts led farmers to send multiple smaller checks with extra insurance.

What We Did:

We leverage the existing Stripe integration for ACH linkage and implemented their digital payment system to replace the cumbersome paper check process. I designed the payment flow to prioritize ease of use and security, with real-time feedback for confidence in processing payments.

Impact:

Reduced fund access time from 5 business days to 2, improving farmers’ ability to act on time-sensitive opportunities.

Before: Mailing a check is the only way to pay back the loan

After: Farmer can make payment on the app with a simplified form anytime, anywhere

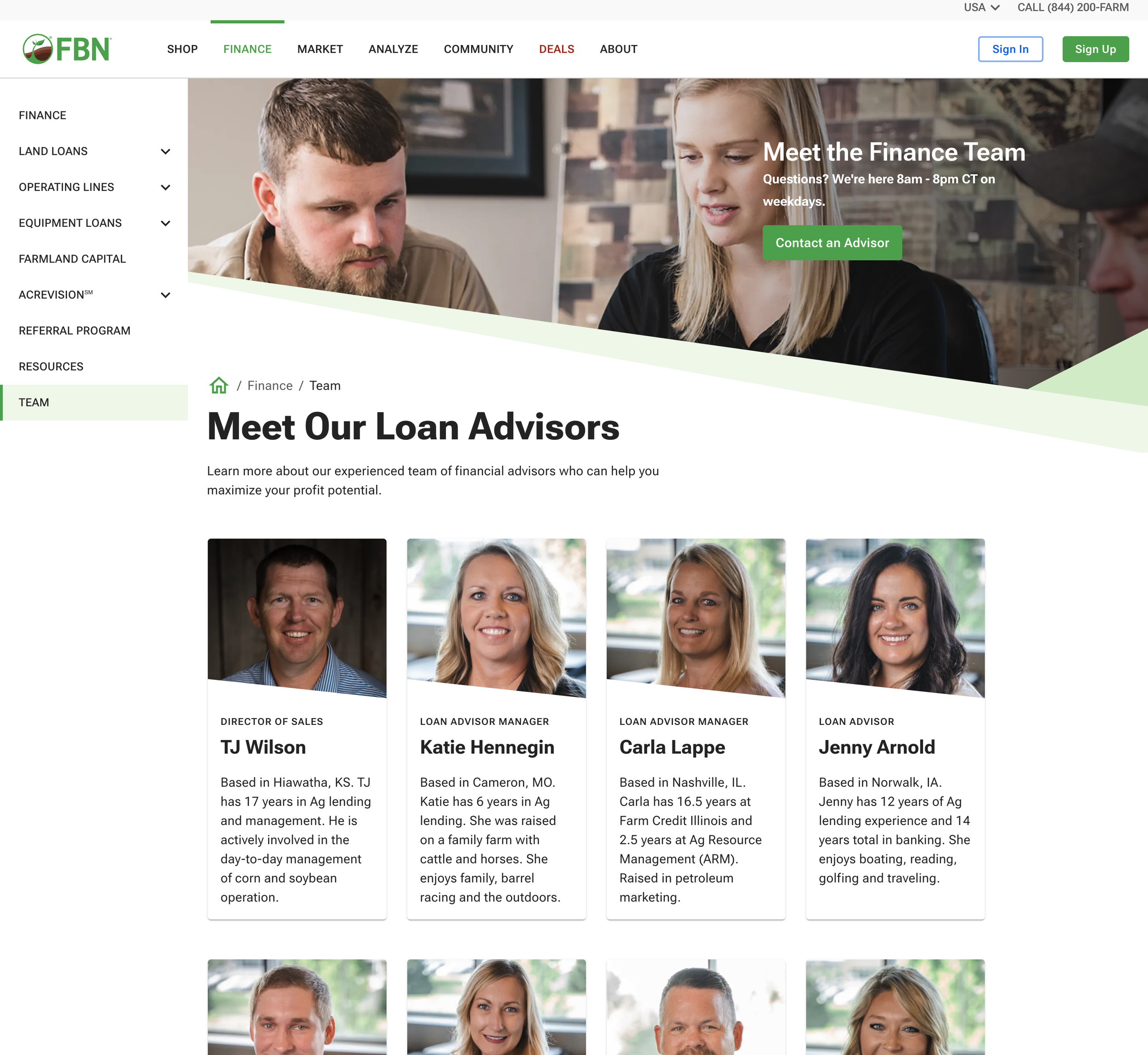

Highlighting Agricultural Expertise in Lending

Research Findings:

Three of our archetypes expressed concerns about lenders lacking agricultural knowledge. Farmers were hesitant to work with lenders and didn't understand their unique challenges such as weather-related delays affecting loan payments. The preferred lenders with a deep understanding of agriculture, as they were more flexible and empathetic.

What We Did:

To address this concern, we worked with marketing to highlight our finance team’s agricultural expertise on our financing pages. We also created a dedicated loan team page, allowing farmers to easily find and connect with their loan advisors. This built trust early in the process and reinforced our focus on personalized, agriculture-specific support.

Balancing Digital Efficiency with Personalized Support

Research Findings:

Our research revealed a distinct divide in communication preferences across archetypes. Strategists and improvers leaned towards a fully digital loan process, valuing efficiency, while rooted and practical farmers preferred more personal, hands-on support. The latter group often had ongoing questions and required additional guidance throughout the loan application process. We needed to balance minimizing human touchpoints for efficiency while ensuring users had easy access to support when needed.

What We Did:

We tailored the loan application process to accommodate both archetypes, ensuring it was self-guided for those who preferred digital interactions but flexible enough for those needing personalized support:

Simplified Collateral Selection: Introduced a map-based tool, allowing farmers to select collateral without need specific details - information that many farmers might not readily have - to reduce confusion.

Optimized Question Flow: Non-essential questions were moved to the end of the application to streamline the initial process. Additional questions were tailored based on their provided information.

Contextual Support: Clear and non-intrusive support information was added throughout the process, ensuring users knew how to contact the FBN Finance team. If a specific advisor was assigned, their contact details were displayed to facilitate direct communication.